“… the real conflict is not between profit maximization and social responsibility…

but rather between short- and long-term thinking.“

As Convenor for ISO 21502 Guidance on Project Management, I am involved in a lot of discussions on projects and project management. I am also fortunate to see the areas of focus and debates from my work with the United Nations and sustainable project management. An area that continues to be discussed is the importance of Asset Life-cycle Benefits.

Over the years, I have noticed conflicting perspectives on “strategy horizons,” particularly between the "East" and the "West":

- the "East" has a reputation for evaluating strategy over decades and centuries; whereas,

- the "West" has a reputation of focusing on the upcoming few quarters until the next bonus round (this is true for both business and governments).

The challenge for Westerners appears to be the ability to understand and focus on the longer term – specifically, longer-term benefits. The West’s short-term focus also applies to projects, where organizations and project teams are more interested in outputs than benefits. Success is claimed too quickly after the new asset is thrown over the wall, and attention / resources are redirected elsewhere before obtaining material benefits from the investment. Though a little tongue in cheek, Exhibit 1 illustrates how easily Western executives are distracted from the longer term perspective:

Exhibit 1: Eleven Second Excerpt from the Disney Film Up

What are Benefits?

First some important definitions that we should keep in mind:

- Benefits: The measurable improvement from change, which is perceived as positive by one or more stakeholders, and which contributes to organizational (including strategic) objectives (Jenner, 2014, page 243).

- Emergent benefits: Benefits that emerge during the design, development, deployment and application of the new ways of working, rather than being identified at the start of the initiative (Jenner, 2014, page 245).

- Dis-benefits: The measurable result of a change, perceived as negative by one or more stakeholders, which detracts from one or more organizational (including strategic) objectives (Jenner, 2014, page 245).

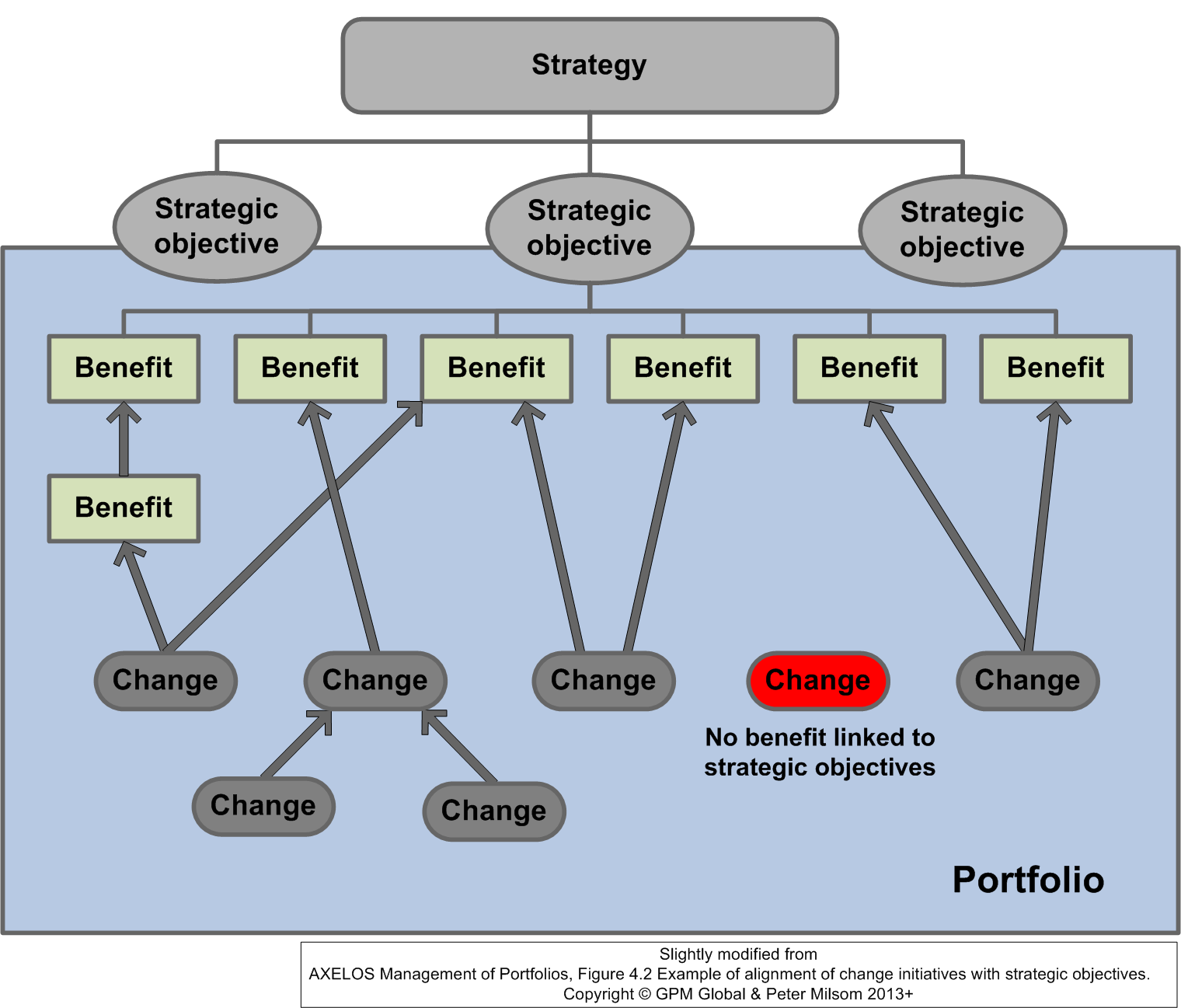

Exhibit 2: Example of alignment of change initiatives with strategic objectives (OGC, 2012)

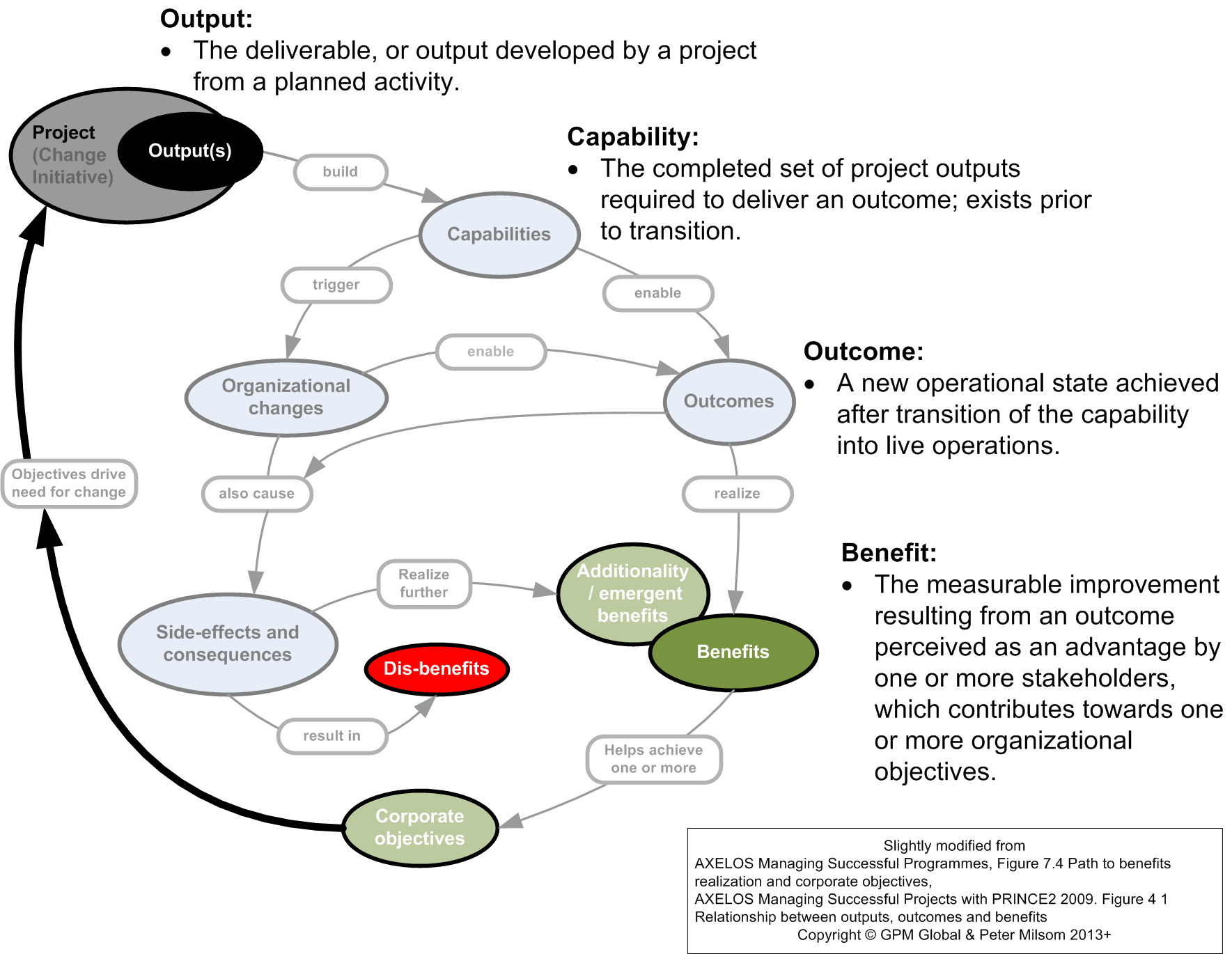

The following modified graphic below is from “Managing Benefits: Optimizing the Return from Investments” Figure 2.1 – Path to benefits realization and corporate objectives Jenner, p 18, 2014. The definitions in the image were taken from Table 2.1 – Outputs, capabilities, outcomes and benefits (Jenner, p 17, 2014). Together they show a realization path for benefits. Exhibit 2 shows this evolution with descriptions, of how corporate objectives become projects that provide outputs that ultimately lead to benefits that fulfill the organizations objectives and the justification for the resource investment. A simplistic definition I often use for project success is did the project obtain the benefits over the life-cycle, in terms of where we currently are and what is planned for in the future, that were modeled in the business case.

Exhibit 3: Path to Benefits Realization and Corporate Objectives

The focus of this image is that for many projects the outputs are one small piece of the puzzle and that benefits realization are the ultimate metric to validate the obtainment of corporate objectives. Personally though, I prefer to use assets instead of outputs.

What are Assets?

I previously discussed Asset Management in the post A Mercenary Perspective on Sustainability, but I feel it is important enough that I provide some context here as well for this topic.

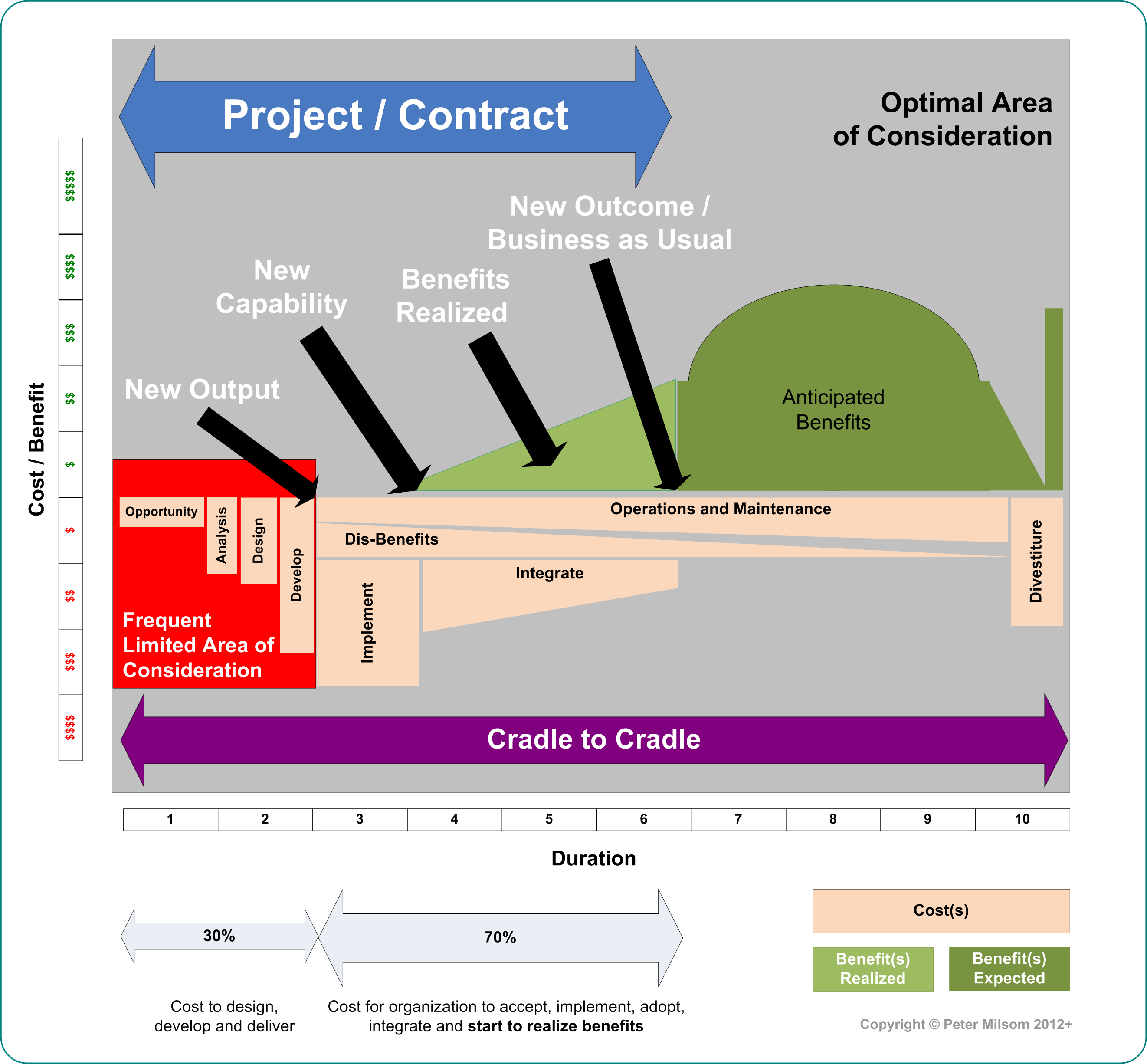

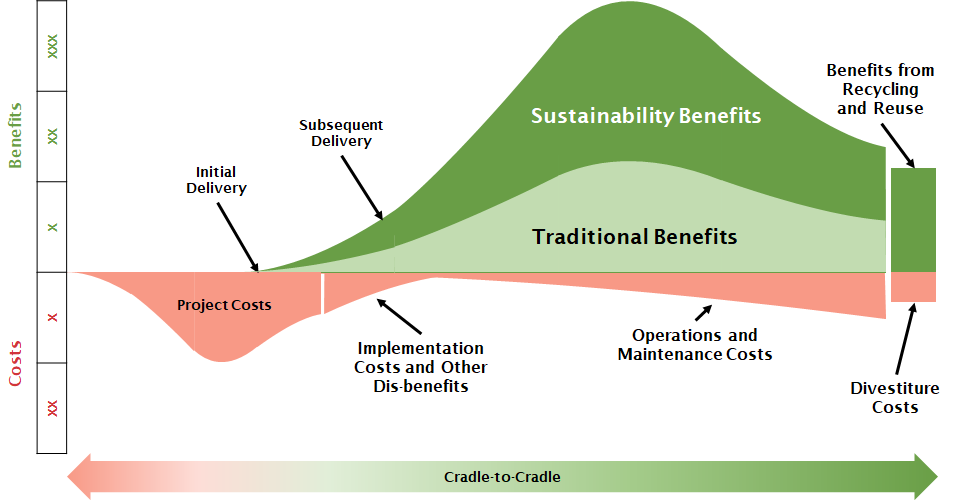

I normally don't show this image because it is so busy, I normally show Exhibit 15, but it provides better insight below. Exhibit 4 provides another project-based asset life-cycle perspective for Exhibit 3 emphasizing where the key milestones take place. An important consideration is a quick review of what an asset is (ISO 55000:2014 Asset management -- Overview, principles and terminology):

Exhibit 4: Cradle to Cradle Asset Life-cycle Benefits Realization Model

The key points of Exhibit 4 are:

- The red box in the lower left hand corner is where most organizations focus. They only care about the output.

- The background grey area is where the organizations should focus... the overall cradle to cradle asset life-cycle perspective to maximize the benefits.

- This image also provides a nice visual representation of what the business case should look like as it evolves over time.

- It is always important to consider the assets financial benefits as well as costs over the life cycle to ensure the asset being invested in is positively worthwhile.

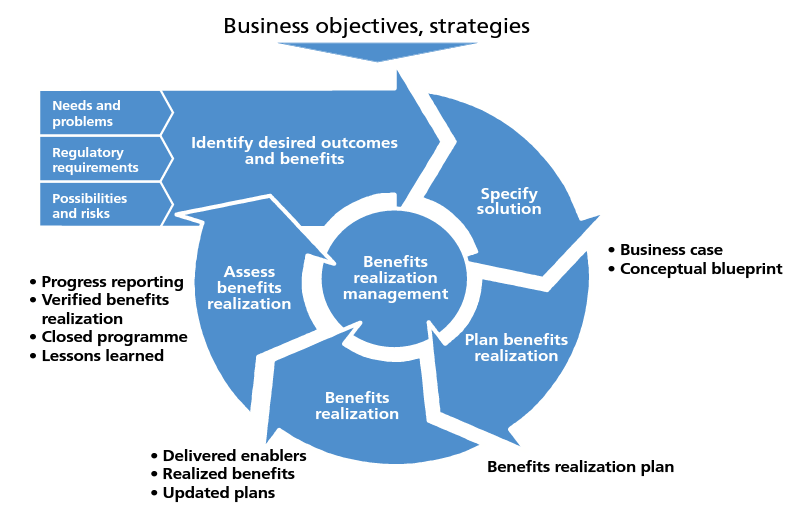

Benefits Realization

Exhibit 5: Swedish e-government delegation benefits model (Jenner, 2014, Figure 3.4)

Another graphic from “Managing Benefits: Optimizing the Return from Investments” Figure 8.2 provides a simple example showing outputs, transition management and benefits realization (Jenner, p 18, 2012).

Exhibit 6: Outputs, Transition Management and Benefits Realization (Jenner, p 18, 2014)

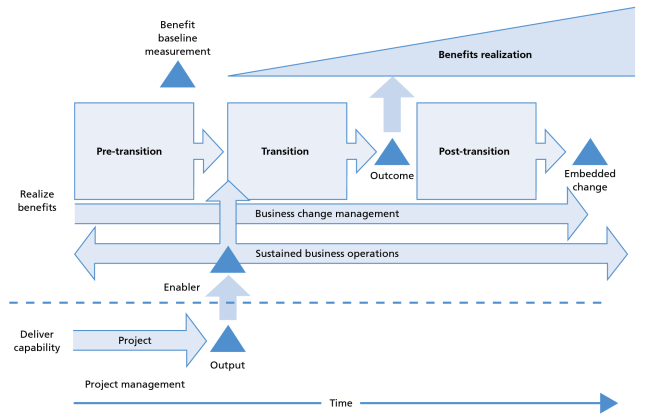

Exhibit 7 from “Managing Benefits: Optimizing the Return from Investments, 2nd Edition” Figure 8.2 Transition management, provides a simpler example (Jenner, p 124, 2014).

Exhibit 7: Transition management (Jenner, p 124, 2014)

We have highlighted what a benefit is

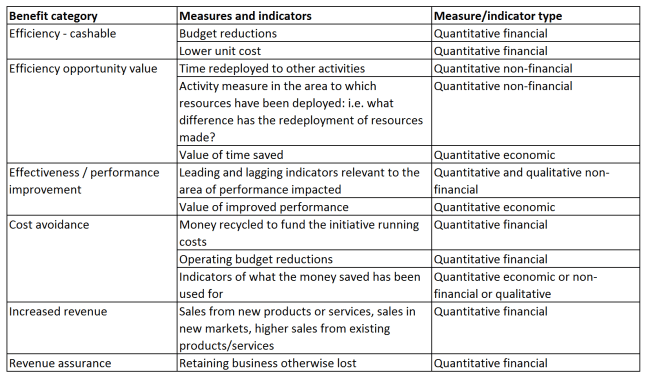

Exhibit 8: Benefits Measurement Taxonomy (Jenner, 2014)

Measuring Benefits

Just for general reading, I often recommend reading Douglas Hubbard's book "How to Measure Anything: Finding the Value of Intangibles in Business," as it is an excellent source for understanding how to properly quantify metrics for business cases and benefits.

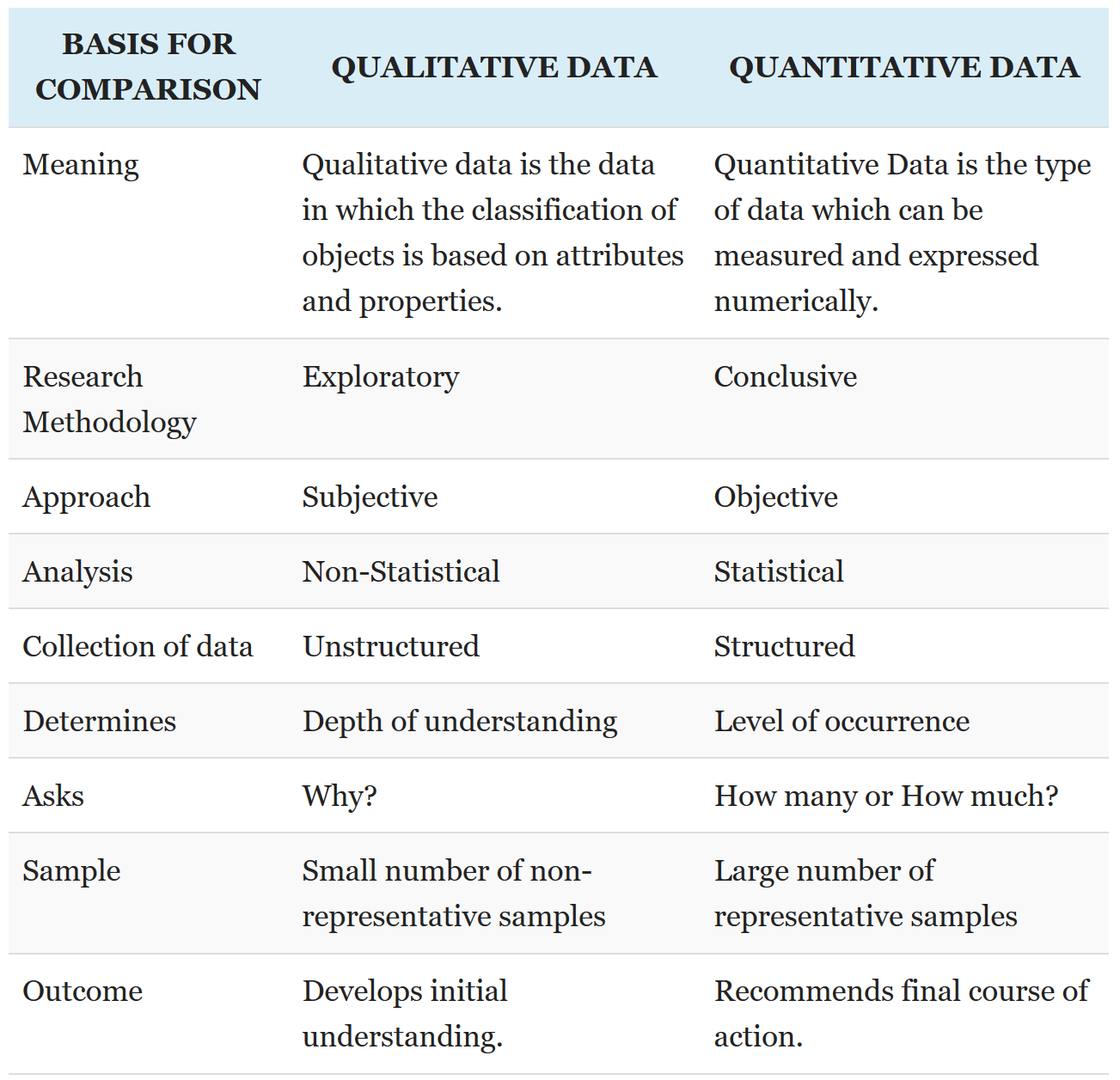

It is important to understand the differences between quantitative and qualitative data and how best to work with them. For business cases and benefits management, we need to ensure we are dealing with quantitative data. The whole purpose of Hubbard's book How to Measure Anything is that we can figure out a way to make anything relevant measurable.

Exhibit 9: Benefits Measurement Taxonomy (Surbhi, 2017)

If organizations are to invest resources, such as time, money and people, while constraints continue to escalate, some due diligence up front becomes a fiscal responsibility. The following was modified from Douglas Hubbard’s book “How to Measure Anything: Finding the Value of Intangibles in Business” (page 8) and discusses decision-making and how relevant information (measurement) supports it:

- Decision makers usually have imperfect information (i.e., uncertainty) about the best choices when making decisions.

- Decisions should be modeled quantitatively because quantitative models have a more favourable track record than unaided expert judgment.

- Business Case Models inform uncertain decisions.

- For any decision or set of decisions, there is a large combination of things to measure and different ways to measure them— but perfect certainty is rarely a realistic option.

- In other words, management needs a method for analyzing its options so as to reduce uncertainty when making decisions.

I would argue that business cases employ various tools and techniques to reduce uncertainty about investment decisions and benefits realization, and provide a framework for prioritization and comparison.

Benefits and Sustainability

In general, the output alone is insignificant, and possibly irrelevant, without benefits. There is a perspective that with (many types of) projects only 30% of the investment is spent on the actual delivery of the output, whereas 70% (often unaccounted for) is spent on the acceptance, adoption and integration of the new or improved assets (services, products or processes) into operations, resulting in the actual benefits the organization expects from the investment.

An interesting way to view this is via the fable of The Goose That Laid the Golden Eggs, the idiom used for an unprofitable action motivated by greed (Covey, p. 52, 2009). The project output delivers a new asset… the goose. The goose has the capability of producing something, with an outcome of golden eggs. The benefit is that you can sell the eggs for money. If you don’t take care of the goose, you lose access to the long-term benefit of generating revenue from selling the eggs.

Exhibit 10: The Goose That Laid the Golden Eggs Idiom

Dealing with benefits for change delivery initiatives forces a long-term, big-picture, sustainable perspective taking into account cost, benefit and risk. Are there other potential benefits that can be supported, or dis-benefits that can be mitigated?

As Exhibit 11 illustrates:

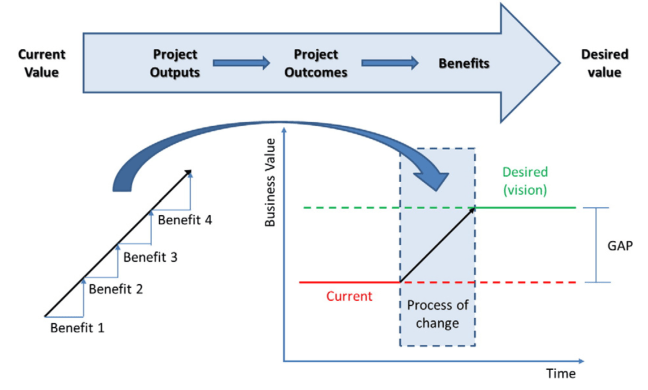

“Initiatives usually fill the value gap by enabling new capabilities – or promoting changes – through the outputs delivered by a set of projects” (Serra et al., p. 55, 2014).

Exhibit 11: Filling the Value Gap (Serra et al., p. 55, 2014)

Responsibility for Benefits

The debate around who is responsible for benefits is always challenging. It is one of the reasons why project management in

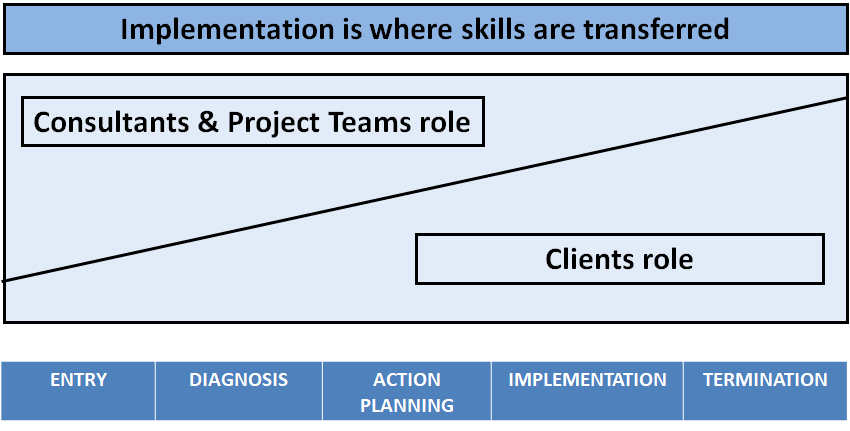

Benefits realization is always the responsibility of the organization and the sponsor... the same as the business case. That said, as demonstrated by this post, management consultants and project teams are in a unique position to help improve benefits and reduce dis-benefits for the asset's overall life-cycle. We can reduce costs such as operations and maintenance, reduce risks, exploit opportunities and generally improve the business case's benefits. It is important though that the organization has been prepared with skills and training to deliver the benefits, as outlined in Exhibit 12.

Exhibit 12: Implementation marks a shift of accountability (CMC Canada)

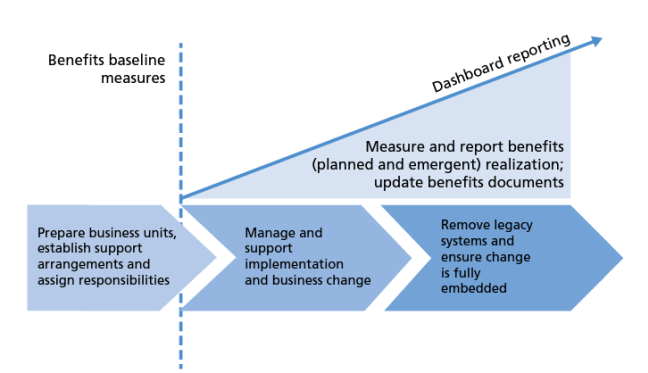

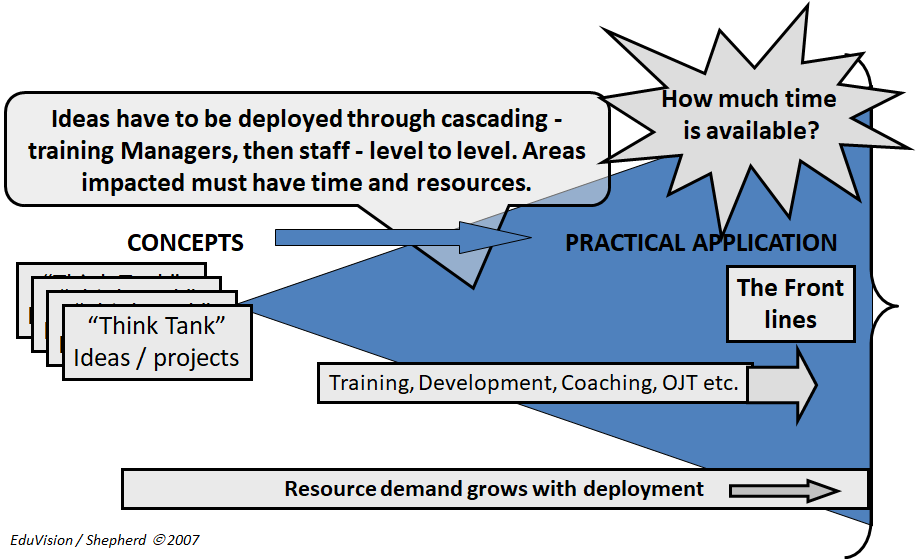

It is also crucial to understand the level of effort to roll out many types of projects change the closer you get to completion for the front lines to be able to deliver the expected benefits, as outlined in Exhibit 13 below. Remember the 30 - 70 rule outlined previously regarding effort for output delivery and effort for the acceptance, adoption and integration to deliver benefits.

Exhibit 13: Organizational capacity for Change (CMC Canada)

The Temporal Nature of Benefits

I find that we often forget to keep in mind that benefits realization depends on when. Do project teams see benefits during the project? Right after the

Exhibit 14 provides another perspective and helps highlight the numerous areas where the project team can aid in the optimal realization of benefits from the project over time.

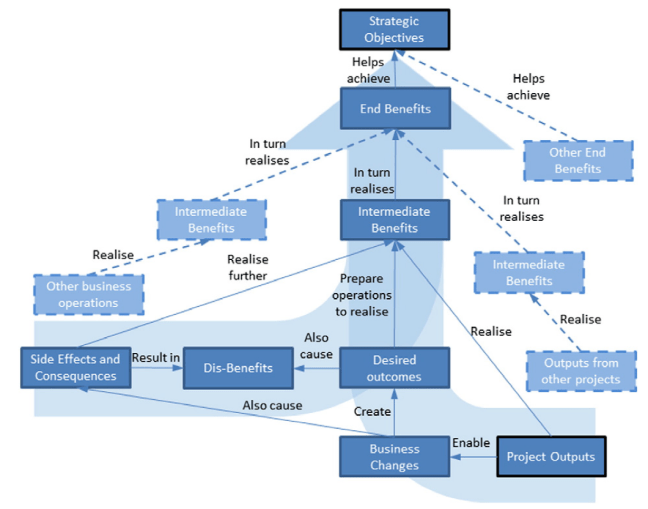

Exhibit 14: Chain of Benefits (Serra et al., p. 56 2014)

A key part of Exhibit 14 is the demonstration of the impact of intermediate benefits, dis-benefits and other benefits that can be enhanced to improve the project. All of these empower greater benefits realization, which is more sustainable.

Once again, it is always valuable to take into account the project's business case and the overall asset life-cycle perspective from cradle to cradle to ensure the benefits realization justification is sound and trending in the right direction. The following image is a simplification of Exhibit 4.

Exhibit 15: Cradle to Cradle (© GPM Global P5, 2017)

Consider the Boiling Frog anecdote. I remember the story of an executive working with a Fortune 100 company in the early 2000s developing strategy. Early on, the corporation was focused on analyzing their strategic horizon over

Conclusion

This post has provided a basic foundation for benefits management and asset management. We started out with a quick review about what benefits and assets are, as well as a number of other definitions, so we are discussing apples to apples and not apples to coconuts. We also reviewed the benefits realization process, and importantly how to make sure that benefits are measurable and hopefully monetary. As with most of my posts, I included a section on sustainability and why benefits are important from a sustainability perspective. The last few sections deal with common challenge areas with benefits, in the area of who is responsible for benefits and the temporal nature of benefits (i.e. when they are measured and what is expected.

For management consultants and project teams, integrating and dealing with the impacts and delivery of benefits provides excellent value for sponsors and their organizations.

PostScript

Just as an interesting follow up to the boiling frog story courtesy of the University of Washington’s Conservation Magazine:

“If you plunge a frog into boiling water, it will immediately jump out. But if you place the frog into cool water and slowly heat it to boiling, the frog won’t notice and will slowly cook to death. So claims the myth. Indeed, everyone—from corporate consultants to politicians to environmental activists—cites the frog fable as proof that people often don’t see change happening and cannot deal with it in the aftermath.

So how did this myth begin? Maybe it arose because frogs are cold-blooded. We

Or perhaps the story began with E.W. Scripture, who wrote The New Psychology in 1897. He cited earlier German research: “. . .

References

- APM. (2011). Delivering Benefits from Investments in Change: Winning Hearts and Minds.

- APM. (2011). Delivering Benefits from Investments in Change: Creating Organisational Capability.

- APM (2012). Delivering Benefits from Investments in Change: An Essential Part of Everyday Business.

- APM (2012). Delivering Benefits from Investments in Change: Beyond ‘Business as Usual’ to ‘Value as Usual’.

- Barton, D. (2011). Capitalism for the Long Term. Retrieved October 9, 2015, from https://hbr.org/2011/03/capitalism-for-the-long-term

- Barton, D., & Wiseman, M. (2014). Focusing Capital on the Long Term. Retrieved October 9, 2015, from https://hbr.org/2014/01/focusing-capital-on-the-long-term/ar/1

- Barton, D., & Wiseman, M. (2015). Book Excerpt: Perspectives on the long term. Retrieved October 9, 2015, from http://www.mckinsey.com/insights/leading_in_the_21st_century/perspectives_on_the_long_term

- Bradley, G.a (2010).

Benefit Realisation Management, Second ed. MPG BooksGroup, UK, Farnham. - Bradley, G. (2010). Fundamentals of Benefits Realisation. TSO.

- Davies H.D. & Davies A.J. (2011). Value Management – Translating Aspirations into Performance. Gower.

- Caccamese, A. (2012). Beyond the Iron Triangle – Year Zero. PMI

- Carboni, J., Duncan, W., Milsom, P., Young, M.Gonzalez, M. (2018) The GPM reference guide to sustainability in Project Management. Fort Wayne: GPM Global, from https://www.amazon.com/Sustainable-Project-Management-Reference-Guide-ebook/dp/B07B8P2VZR/ref=sr_1_fkmr0_1?keywords=Sustainable+Project+Management+-+The+GPM+Reference+Guide%2C+2nd+Edition&qid=1558391086&s=gateway&sr=8-1-fkmr0

- Carboni, Joel (2017). The GPM P5™ Standard for Sustainability In Project Management. 2nd ed. Fort Wayne: GPM Global.

- Conner Partners (2004). The Leader’s Challenge: Installation or Realization.

- Covey, Stephen R. (2009). The 7 Habits of Highly Effective People. RosettaBooks.

- GAPPS (2015). A Guiding Framework for Project Sponsors. Global Alliance for Project Performance Standards.

- GPM. (2012). PRISM PRojects Integrating Sustainable Methods. Green Project Management Association.

-

Hubbard, Douglas W. How to Measure Anything: Finding the Value of "Intangibles" in Business. John Wiley & Sons, 2014, from https://www.amazon.ca/How-Measure-Anything-Intangibles-Business/dp/1118539273/ref=sr_1_1?crid=297WT5PVGIP7E&keywords=how+to+measure+anything&qid=1558390758&s=gateway&sprefix=how+to+measure+anything%2Caps%2C173&sr=8-1#reader_1118539273

- ISO. (2014). ISO 55000:2014 – Asset management: Overview, principles and terminology. Retrieved October 9, 2015, from http://www.iso.org/iso/home/store/catalogue_tc/catalogue_detail.htm?csnumber=55088

- ISO. (2014). ISO 55001:2014 – Asset management: Management systems — Requirements. Retrieved October 9, 2015, from http://www.iso.org/iso/home/store/catalogue_tc/catalogue_detail.htm?csnumber=55089

- ISO. (2014). ISO 55002:2014 – Asset management: Management systems — Guidelines for the application of ISO 55001. Retrieved October 9, 2015, from http://www.iso.org/iso/home/store/catalogue_tc/catalogue_detail.htm?csnumber=55090

- Jenner, S. (2011).

Realising Benefits from Government ICT Investment – A Fool’s Errand? Academic Publishing. - Jenner, S. & APMG-International (2012). Managing Benefits: Optimizing the Return from Investments, 1st Edition. The Stationery Office.

- Jenner, S. & APMG-International (2014). Managing Benefits: Optimizing the Return from Investments, 2nd Edition. The Stationery Office.

- Kern, M. (2014). Outcomes vs Capabilities. Retrieved October 8, 2015, from https://www.linkedin.com/pulse/20140919090447-86002769-outcomes-vs-capabilities?trk=hb_ntf_MEGAPHONE_ARTICLE_POST&trk=hb_ntf_MEGAPHONE_ARTICLE_POST

- Kruszelnicki, Dr. Karl S. (2011). Frog Fable Brought to Boil. Retrieved January 1, 2016, from http://conservationmagazine.org/2011/03/frog-fable-brought-to-boil/

- Mills-Scofield, D. (2012). It’s Not Just Semantics: Managing Outcomes Vs. Outputs. Harvard Business Review.

- OGC – The Office of Government Commerce (2009). Managing Successful Projects with PRINCE2™ 2009. The Stationary Office. http://www.amazon.com/gp/product/0113310595?keywords=prince2&qid=1444246966&ref_=sr_1_1&sr=8-1

- OGC – The Office of Government Commerce (2012). Management of Portfolios. The Stationary Office. http://www.amazon.com/Management-Portfolios-Book-Best-Practice/dp/0113312946/ref=sr_1_1?s=books&ie=UTF8&qid=1442811531&sr=1-1&keywords=Management+of+Portfolios

- PROSCI (2010). Viking Ship Tutorial – Which sounds more like your projects?.

- Remenyi, D., Bannister, F. & Money, A. (2007). The Effective Measurement and Management of ICT Costs and Benefits, 3rd edition. Elsevier.

- Rowe, W. G., & Nejad, M. H. (2009). Strategic Leadership: Short-Term Stability and Long-Term Viability. Ivey Business Journal, (September / October). Retrieved from http://iveybusinessjournal.com/publication/strategic-leadership-short-term-stability-and-long-term-viability/

- Schroeder, C. M. (2014). Let’s Fix It: The Rest of the World Is Rising With or Without the West. Retrieved October 8, 2015, from https://www.linkedin.com/pulse/20141016120343-18642888-let-s-fix-it-the-rest-of-the-world-is-rising-with-or-without-the-west

- Serra, C.E.M. & Kune, M. (2014). Benefits Realisation Management and its influence on project success and on the execution of business strategies. International Journal of Project Management, 33 (2015) 53–66.

- Simms, J. (2011). Solving the Benefits Puzzle. Totally Optimized Projects.

- Stephenson, H. Lance. (2015). TCM Framework, Second Edition. Retrieved October 9, 2015, from http://www.aacei.org/resources/tcm/

-

Surbhi S. “Difference Between Qualitative and Quantitative Data (with Comparison Chart).” Key Differences, 3 Nov. 2017, keydifferences.com/difference-between-qualitative-and-quantitative-data.html.

- Thiry, M. (2002). Combining value and project management into an effective programme management model. International Journal of Project Management. 20, 221–227

- Thorp, J. and Fujitsu Consulting’s Center for Strategic Leadership (2003). The Information Paradox – Realizing the Business Benefits of Information Technology. McGraw-Hill, Canada.

- Usher, G. (2014). Paper – Rethinking Project Management theory: A case for a paradigm shift in the foundational theory of client-side construction project management.

- Usher, G. (2015). Presentation – Rethinking Project Management theory: A case for a paradigm shift in the foundational theory of client-side construction project management.

- Vermeulen, F. (2015). 5 Strategy Questions Every Leader Should Make Time For. Retrieved October 8, 2015, from https://hbr.org/2015/09/5-strategy-questions-every-leader-should-make-time-for

- Ward, J. & Daniel, E. (2012). Benefits Management – How to Increase the Business Value from Your IT Projects. Wiley.

- Wessel, M. (2014). The Most Innovative Companies Have Long-Term Leadership. Retrieved October 8, 2015, from https://hbr.org/2014/12/the-most-innovative-companies-have-long-term-leadership

About the Author - Peter Milsom, FCMC, GPM Global

Peter Milsom helps organizations understand what sustainability means to them, to maximize their benefits and value while minimizing costs and threats. He does this by helping organizations at all levels from the c-suite to the front lines understand what all of the elements of sustainability are, and helping them prioritize and focus on those areas that make the most sense. His area of focus in the sustainability space is change delivery or projects. Peter has also worked on several international standards, and is currently the Convenor of ISO 21502 Guidance on Project Management, and is the Secretary of the ISO 31000 Implementation Guidance Handbook. Peter is currently a Board Member of CMC-Ontario.

He is a contributing author: Sustainable Project Management - The GPM Reference Guide, 2nd Edition; The GPM P5 Standard for Sustainability in Project Management v1.5.

A version of the article was first published here.